What is workers’ compensation insurance, who needs it, and what does it cover?

When you have workers’ compensation insurance and employee injuries or illnesses occur, you’ll have the peace of mind to know your business is properly covered and can provide your employee with the help they need. Also, when sufficient workers’ compensation insurance is purchased, employers cannot be held liable for employee injuries in most states, except in very few circumstances. However, wage replacement expenses, medical bills, vocational rehabilitation, legal fees, and any other additional costs can get quite expensive when insurance coverage is not sufficient. That’s where making sure you have the right kind of policy comes in.

Almost all states require workers’ compensation insurance for companies with employees – and even for some without employees

Required by nearly every state in the U.S. since 1911, workers’ compensation insurance can now vary significantly according to each state’s laws and regulations. It can also range widely based upon how many employees you have and what type of work your business does. So how can a business owner figure out where to start? Let’s take a look.

You must fully understand your state’s requirements

Since workers’ compensation insurance is regulated by the states, getting to know the details on your state’s requirements and penalties is essential for every business owner. Policy premiums can range considerably depending upon your payroll costs, industry type, employees’ job risk classifications, and state, so it’s important for business owners to get the facts.

There are over 700 business classification codes, which impact your premium

The National Council on Compensation Insurance, or NCCI, is a rating bureau which oversees Workers’ Compensation issues throughout the country, assigning categorization codes to the work each business does. These codes correspond to the risks associated with performing that type of work according to the latest research. The greater the risk of injury, the higher the costs of workers’ compensation insurance. The NCCI also determines the experience modification factor, of MOD, which represents your company’s claim history as a number, and results in a likely adjustment made in the form of a credit or debit on your insurance policy. A low number of claims often translates into a lower premium. For companies with the fewest claims or least severe accidents, the MOD is less than 1.00

How are workers’ compensation insurance rates calculated?

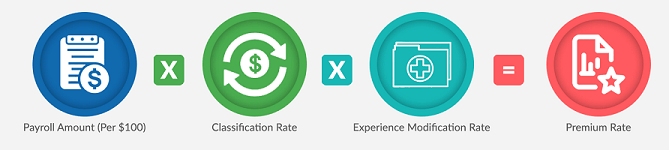

Additionally, the NCCI gathers data and creates most, but not all, state manuals on the method of premium computation — which can sometimes be difficult to understand. Some states have independent rating bureaus or “stand-alone” rating bureaus that are not associated with the NCCI as well. And, so, as you may have guessed, the costs of workers’ compensation insurance premiums can range broadly depending on these bureaus’ methods and codes. Generally, workers’ compensation insurance premiums are calculated according to their classification code and the rate assigned to it, and expressed in terms of every $100 of payroll costs for each classification code. This essentially comes down to:

Payroll amount (per $100) multiplied by classification rate multiplied by the experience modification rate equals the premium rate

This chart can also give you an idea of the premium range possible depending on work types and codes from the June 2017 Bureau of Labor Statistics.

Acceptable forms of workers’ compensation insurance vary by state as well

Obtaining workers’ compensation insurance through one of the likely hundreds of private insurance carriers in your state, purchasing a policy from a public insurance carrier or state fund, joining a safety group, or becoming authorized for individual, group, or local government self-insurance are all ways to get the coverage your business needs in your state – and our site can help you get the relevant information you need for your state instantly. Since there’s no single, cohesive method to easily calculating premiums, coverage, or benefits for each state, it helps to get assistance from a site like ours.

Tips your company may find useful in reducing policy premiums include:

Stay ahead of the game – by several months

Getting and comparing accurate quotes several months before you know you’ll actually need the policy to become effective. (Our team can do that for you on this site as well.)

Always be honest

Be honest about your employee job classifications. If you attempt to lower costs by misclassifying this information initially, you’ll likely be caught in an audit and get charged the full amount retroactively anyway — in addition to any penalties your state has in place for this crime, which often include hefty fines and even criminal penalties as serious as felony prosecution in some cases.

Look for ways to lower premiums or potential claim costs

Get clarity on which alternatives are available for your business in your state including premium credits, deductibles, safety programs, etc. Improving your company’s work environment to be as safe as possible and taking steps to lower potential losses can help keep premiums low and possibly lower your claim costs in the event of an injury/illness as well.

Get the skinny on claims processing

Find out how claims are processed by your potential insurer/s. The procedure in place may actually affect your premium more directly than you realize!

Find out details on contractors/subcontractor requirements

Be sure you understand what you need for or from any contractors or subcontractors working for your company. If the contractors/subcontractors provide their own workers’ compensation insurance, employers may only need to request a copy of their certificate of insurance for the policy. Once obtained, these certificates may help employers to lower company’s workers’ compensation premiums.

Be sure you keep accurate, up-to-date records

Most likely, annual audits on workers’ compensation insurance policies will be conducted to ensure the initial information reported has been properly updated. Changes in your business operation, payroll, or classifications must be adjusted for an accurate final audit premium. This may result in a refund being made to you, an additional balance due, or other types of changes in your policy.

Keep in mind some information may be (or become) publicly available

In some states, workers’ compensation records may be made available to the public by request per the Freedom of Information Act or other similar laws. In such cases. requests can be made for records in person, by mail, or via email to the state workers’ compensation office. Records may be made available for inspection or copying or both, and any further regulations pertaining to either are usually posted on the department website or in their office.